Flexible Spending Accounts (FSA)

Brown & Brown and Proctor Loan Protector Teammates.

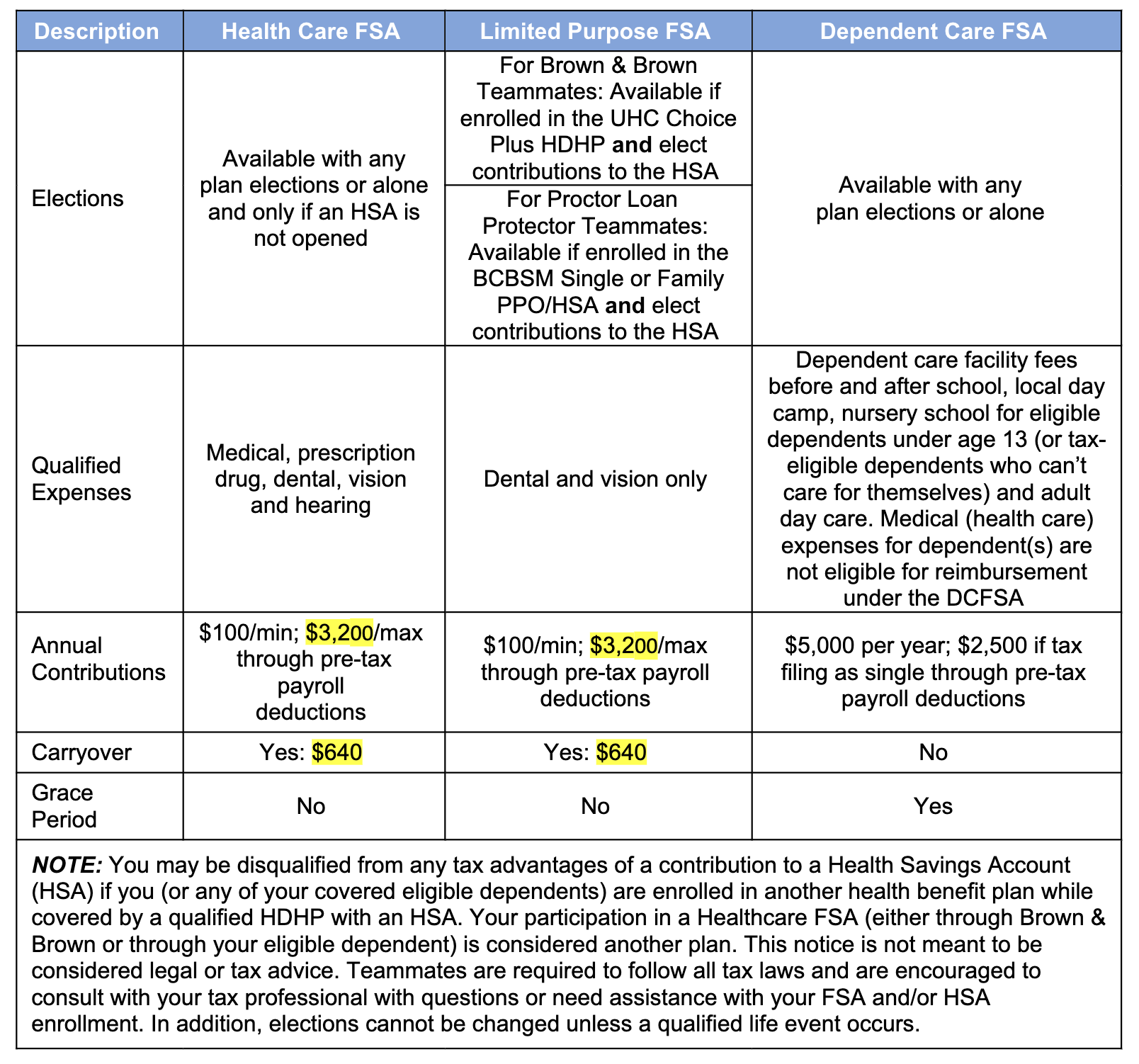

Brown & Brown provides you with the opportunity to pay for eligible medical, dental, vision, and dependent care expenses on a pre-tax basis with flexible spending accounts (FSAs). Administrative services and claim reimbursements for the Health Care FSA (HCFSA), Limited Purpose FSA (LPFSA) and Dependent Care FSA (DCFSA) are provided by HealthEquity/WageWorks.

The Flex Plan Year is January through December. Eligible expenses must be incurred by December 31st to be qualified for reimbursement in the current Plan Year. Eligible expenses incurred during the Flex Plan Year must be submitted by the following March 31st. It is important to choose your annual amount(s) carefully to avoid any unused funds at the close of the Plan Year.

Health Care FSA (HCFSA) and Limited Purpose FSA (LPFSA):

- The HCFSA and LPFSA includes a carryover provision up to $640 (IRS max allowed, subject to change). Any remaining funds in a HCFSA or LPFSA at the end of the Plan Year will have up to $640 of unused funds carry over which can be used for eligible expenses incurred in following Plan Year. Any unused funds over and above $610 will be forfeited. For example, if $3,200 was contributed to the FSA and only $2,000 of eligible expenses were incurred, $640 would carry over but the remaining unused funds would be forfeited.

- The HCFSA and LPFSA can be reimbursed up to the total amount elected to deposit for the year. If termination of either benefit occurs prior to the end of the Plan Year, you are only eligible for reimbursement of expenses which were incurred while you were a participant in the Plan unless (if applicable) COBRA continuation is elected.

Dependent Care FSA (DCFSA):

- Includes a 2½ month grace period which allows for eligible DCFSA expenses to be incurred after the end of the Plan Year. You will have until March 15th of the following year to incur new expenses and use money left in your DCFSA. The last day to submit claims is March 31st. Any unused funds would be forfeited after the grace period ends.

- The DCFSA can be reimbursed up to the total amount deposited in your account. If termination of the DCFSA occurs prior to the end of the Plan Year, you can continue to request eligible reimbursements until the earlier of the date your balance is exhausted or the end of the Plan Year. Medical (health care) expenses for your dependent(s) are not eligible for reimbursement under the Dependent Care FSA.

HealthEquity Debit Card:

- A HealthEquity Health Care Visa® debit card is issued for the HCFSA and LPFSA and is mailed to your home address by HealthEquity/WageWorks. It can be used to pay for qualified expenses and is limited to the eligible expenses associated with the plan. For a full list of qualified expenses allowed by the IRS, refer to Publication 502 at irs.gov. Keep all receipts for reference.

- IMPORTANT NOTE: The Health Care debit card cannot be used for eligible dependent care expenses. Expenses for DCFSA can be submitted through the member portal on the HealthEquity/WageWorks website, completion of a DCFSA reimbursement form, or through the HealthEquity/WageWorks mobile app. Recurring DCFSA claims can be scheduled for the duration of the Plan Year. Reimbursements will be made through direct deposit to an account specified by you.

IMPORTANT DOCUMENTS:

Hawaii Teammates

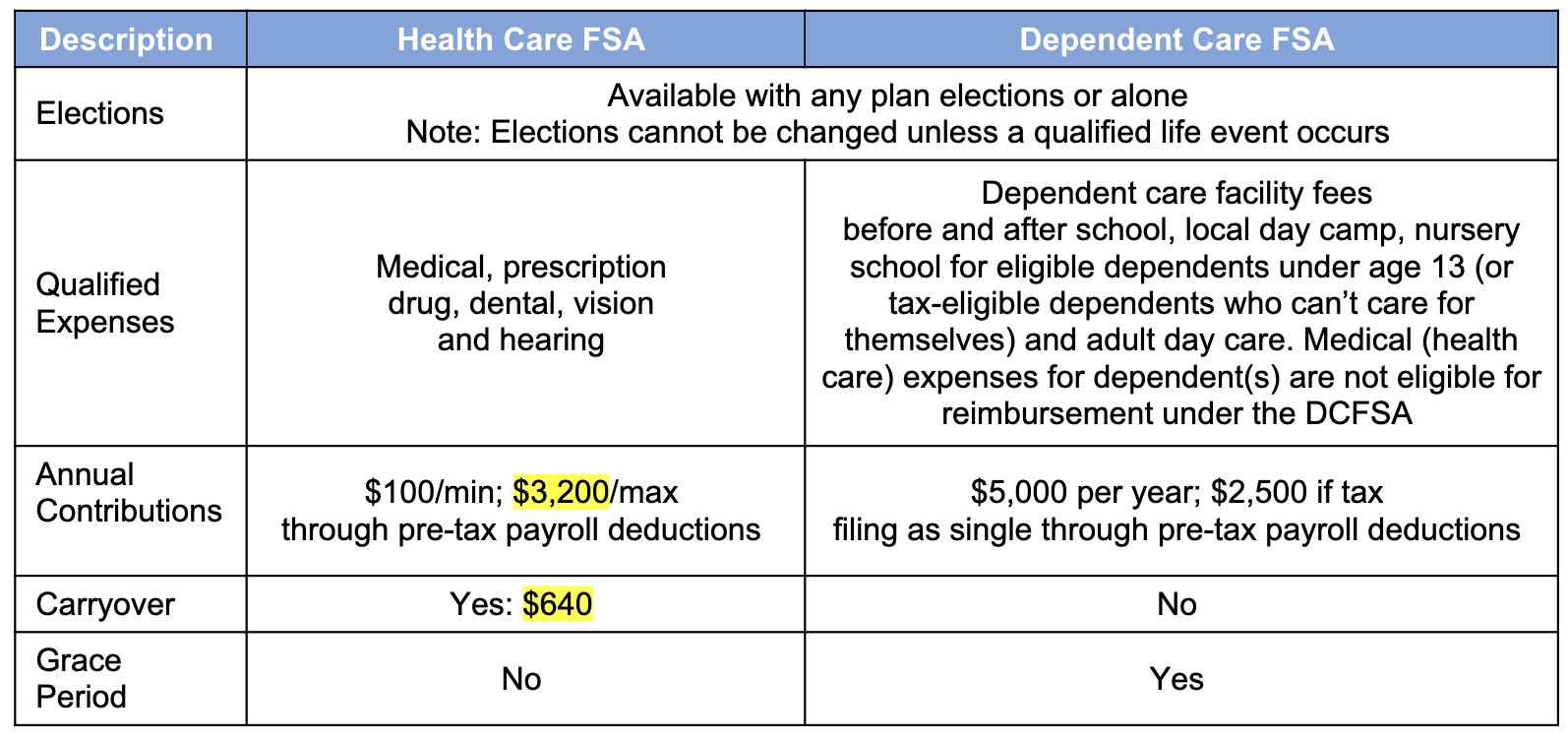

Brown & Brown provides you with the opportunity to pay for eligible medical, dental, vision, and dependent care expenses on a pre-tax basis with flexible spending accounts (FSAs). Administrative services and claim reimbursements for the Health Care FSA (HCFSA), and Dependent Care FSA (DCFSA) are provided by HealthEquity/WageWorks.

The Flex Plan Year is January through December. Eligible expenses must be incurred by December 31st to be qualified for reimbursement in the current Plan Year. Eligible expenses incurred during the Flex Plan Year must be submitted by the following March 31st. It is important to choose your annual amount(s) carefully to avoid any unused funds at the close of the Plan Year.

Health Care FSA (HCFSA):

- The HCFSA includes a carryover provision up to $640 (IRS max allowed, subject to change). Any remaining funds at the end of the Plan Year will have up to $640 of unused funds carry over which can be used for eligible expenses incurred in following Plan Year. Any unused funds over and above $640 will be forfeited. For example, if $3,200 was contributed to the FSA and only $2,000 of eligible expenses were incurred, $640 would carry over but the remaining unused funds would be forfeited.

- The HCFSA can be reimbursed up to the total amount elected to deposit for the year. If termination of either benefit occurs prior to the end of the Plan Year, you are only eligible for reimbursement of expenses which were incurred while you were a participant in the Plan unless (if applicable) COBRA continuation is elected.

Dependent Care FSA (DCFSA):

- Includes a 2½ month grace period which allows for eligible DCFSA expenses to be incurred after the end of the Plan Year. You will have until March 15th of the following year to incur new expenses and use money left in your DCFSA. The last day to submit claims is March 31st. Any unused funds would be forfeited after the grace period ends.

- The DCFSA can be reimbursed up to the total amount deposited in your account. If termination of the DCFSA occurs prior to the end of the Plan Year, you can continue to request eligible reimbursements until the earlier of the date your balance is exhausted or the end of the Plan Year. Medical (health care) expenses for your dependent(s) are not eligible for reimbursement under the Dependent Care FSA.

HealthEquity Debit Card:

- A HealthEquity Health Care Visa® debit card is issued for the HCFSA and is mailed to your home address by HealthEquity/WageWorks. It can be used to pay for qualified expenses and is limited to the eligible expenses associated with the plan. For a full list of qualified expenses allowed by the IRS, refer to Publication 502 at irs.gov. Keep all receipts for reference.

- IMPORTANT NOTE: The Health Care debit card cannot be used for eligible dependent care expenses. Expenses for DCFSA can be submitted through the member portal on the HealthEquity/WageWorks website, completion of a DCFSA reimbursement form, or through the HealthEquity/WageWorks mobile app. Recurring DCFSA claims can be scheduled for the duration of the Plan Year. Reimbursements will be made through direct deposit to an account specified by you.

IMPORTANT DOCUMENTS:

Health Savings Accounts (HSA)

Brown & Brown Teammates

A Health Savings Account helps you save money to pay for future eligible health care expenses.

Health Savings Account (HSA):

- Administered by Optum Bank.

- HSA is available for teammates enrolled in the Choice Plus High Deductible Health Plan (HDHP) – if elected, you will receive a newly established HSA automatically opened by Optum Bank.

- No monthly fee for the basic Optum Bank HSA. Fees apply when investment options are elected.

- HSA investment options are available when the basic account exceeds $1,000.

- Welcome Kit and Mastercard® Debit Card mailed from Optum Bank.

- No “use it or lose it” policy – account is owned and managed by you.

- IMPORTANT: Be sure to complete beneficiary information for your HSA.

Access and manage your HSA through the UnitedHealthcare (UHC) site at myuhc.com or Optum Bank at optumbank.com where you can view your account balance, set-up to transfer funds, pay bills, check deposits and withdrawals.

Eligibility:

If you enroll in the Choice Plus HDHP, you can also elect an HSA. However, under IRS rules you are not eligible for an HSA if you claimed as a dependent on someone else’s tax return or if you enrolled in any other non-qualified medical coverage. This includes:

- Your or your spouse’s Health Care Flexible Spending Account (HCFSA).

- Medicare Part A or B.

- TRICARE, TRICARE for Life or Veterans Administration medical benefits (unless you have a service-connected disability.

- Short-term travel medical insurance that provides coverage when you travel outside the U.S. (whether or not provided by Brown & Brown).

- Consult with your tax professional with questions.

Contribution Limits:

- $4,150 for single coverage.

- $8,300 for family coverage.

- $1,000 catch-up contribution if 55 or older and can begin any time in the calendar year in which you will reach age 55 (applies to primary account holder).

- Changes to amount can be requested monthly in Workday. The more you can set aside, the more your money will grow over time.

Important Documents:

Download the Optum Bank mobile app to view your account information

Proctor Loan Protector Teammates

A Health Savings Account helps you save money to pay for future eligible health care expenses.

Health Savings Account (HSA):

- Available when enrolled in the BlueCross Blue Shield of Michigan (BCBSM) Simply Blue PPO/HSA Plan.

- HealthEquity is the HSA provider and is fully integrated with BCBSM. You can manage your HSA through the BCBSM portal at bcbsm.com or on the BCBSM mobile app.

Eligibility:

If you enroll in the BlueCross BlueShield of Michigan (BCBSM) Simply Blue PPO/HSA Plan, you can also elect an HSA. However, under IRS rules you are not eligible for an HSA if you claimed as a dependent on someone else’s tax return or if you enrolled in any other non-qualified medical coverage. This includes:

- Your or your spouse’s Health Care Flexible Spending Account (HCFSA).

- Medicare Part A or B.

- TRICARE, TRICARE for Life or Veterans Administration medical benefits (unless you have a service-connected disability.

- Short-term travel medical insurance that provides coverage when you travel outside the U.S. (whether or not provided by Brown & Brown).

- Consult with your tax professional with questions.

Contribution Limits:

- $4,150 for single coverage.

- $8,300 for family coverage.

- $1,000 catch-up contribution if 55 or older and can begin any time in the calendar year in which you will reach age 55 (applies to primary account holder).

- Changes to amount can be requested monthly in Workday. The more you can set aside, the more your money will grow over time.

IMPORTANT DOCUMENTS:

HSA vs Health Care & Limited Purpose FSA Overview

HSA Advantages:

- Owned and managed by you; follows you wherever you go.

- Accumulated balance that can also be used for:

- COBRA premiums.

- Certain coverage for Medicare eligible employees.

HSA Tax Advantages:

- Contributions deposited pre-tax through payroll deductions.

- Withdrawals for eligible medical expenses are not taxable.

NOTE: You may be disqualified from any tax advantages of a contribution to a Health Savings Account (HSA) if you (or any of your covered eligible dependents) are enrolled in another health benefit plan while covered by a qualified HDHP with a HSA. Your participation in a Healthcare FSA (either through Brown & Brown or through your eligible dependent) is considered another plan. This notice is not meant to be considered legal or tax advice. Teammates are required to follow all tax laws and are encouraged to consult with your tax professional with questions or need assistance with your FSA and/or HSA enrollment.